Background

As a tenant advisor, one of the most important services we provide is to ensure our clients receive best-in-class representation in securing lease terms which exceed market conditions. Just getting a transaction done is simply not good enough; getting it done right throughout every phase of the process while eliminating surprises is what differentiates a quality broker.

Before diving into the details of a net effective return analysis, it’s important to understand there are many variables that need to be taken into consideration on any lease negotiation. These may include, but are not limited to, the following:

- Flexibility to grow or contract

- Renewal or early termination rights

- Tenant improvement allowances

- Moving allowances

- Rental concessions

- Annual escalation factors for net rent

- Net rates

- Exclusions or caps on operating costs and taxes

- Project management fees, if any, that landlord may charge

- Market definitions for renewal options

- Parking costs and/or concessions

- Amenity packages

- Signage rights

- Improvement to building common areas

- Lease commissions

- Stability of ownership

- Quality of property management

Individual landlord motivation may also vary greatly from owner to owner. This can be impacted by plans, or the need, to refinance, as well as a desire to position an asset for sale. Identifying these unique and ancillary motivations can also produce significant results if identified and understood prior to negotiation terms.

While the balance of this article will focus on economic returns, keep in mind there are many other factors that should not be overlooked such as:

- Quality of the property management team

- Landlord’s reputation for maintaining their asset

- Whether the landlord is a long-term owner, or likely to sell

- Landlord’s financial strength

With all of this background we are now ready to focus on using net effective landlord returns as a tool in negotiating leases that reflect or exceed market conditions.

Assessing the Data

In order to compare a deal to the market, one must have access to quality data. Maintaining a database of relevant transaction comps is critical. Comps need to include details on all variables which drive landlord returns; this includes average net rental rates over the term of the lease, as well as landlord concessions such as tenant improvement allowances, free rent, and commissions. A comp that is six to twelve months old may not be relevant if market conditions have changed. Space absorption, as well as any change in economic conditions can also influence perceptions and affect reality regarding market sentiment. For this reason, one of my favorite lines is “reality is important, but perception is everything,” as it is perception that will often drive the market at the micro level. An example snapshot of lease comps showing landlord net effective returns is included below for illustration purposes:

When we model landlord net effective return, we’re simply looking at the transaction from a landlord’s perspective. To calculate a net effective return, take the total net rent paid to the landlord over the life of the lease and deduct for all Landlord out-of-pocket costs. These out-of-pocket costs primarily include tenant improvement allowances, rental concessions and brokerage commissions. Whether we wish to apply an interest factor to these amortized costs is optional, but the bottom line is to come up with a net effective landlord return that can be compared to other landlord net effective returns to determine market. Looking at the averages of the market comps provides a sense of typical concessions and allowances to assist in negotiating final terms.

For our purpose we will not apply any interest factor for relevance in comparison. If we wanted to see if a particular transaction covered debt service cost for a landlord we would consider an appropriate interest factor, but the key is to compare all proposed returns on our most relevant lease comps to determine a range for negotiations and measure results relative to market so that final terms can be recommended and negotiated to conclusion.

Ideally we will have at least 10-12 relevant comps with a predetermined landlord net effective return to provide a range for final comparison to our short listed properties (typically 3-5) for proposal comparison and one final selection. This method of comparing alternate terms is especially useful in finalizing terms after modifying different elements of the proposal and running the new landlord net effective return.

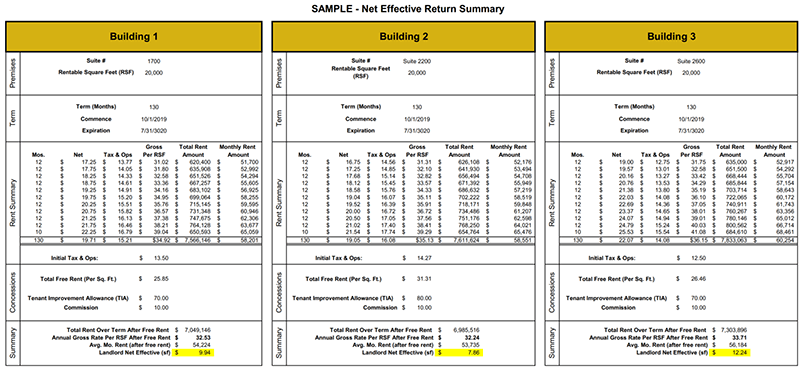

The illustration below summarizes landlord net effective returns calculated for three select properties. By comparing these to our comp data, we can see that economic terms offered by Building 2 have exceeded market conditions.

Conclusion

Analyzing landlord net effective returns shows progress made in negotiations from the initial proposal to the completion of a fully negotiated lease. It also confirms final terms relative to market which gives our clients the confidence to know they have gotten a great lease result negotiated diligently on their behalf which is supported by solid market comps.

About the Author

TaTonka Real Estate advisors is a team of commercial real estate experts that focus exclusively on serving tenants and buyers across all industries and is headquartered in Minneapolis, Minnesota.

Steve Chirhart is a founding partner of TaTonka and has served clients locally and nationally for over three decades. His areas of specialization include office, industrial, build-to-suit, investment, land, medical and retail transactions. Steve holds the Society of Industrial and Office Realtors (SIOR) designation and is a past president of the Minnesota Commercial Board of Realtors and the local SIOR chapter.